This is the second in a series of memos that we wrote to sharpen our perspective on COVID-19’s impacts on the U.S. labor market and begin to define the implications for Braven’s programming and support of Fellows. Click here for our first post on learnings about the job market from past recessions.

Braven seeks to scale its impact and support more underrepresented college students – first-generation students, students from low-income backgrounds, and students of color – nationally. The objective of this memo is to understand the latest trends in college enrollment and persistence and how these are impacted by COVID-19 and persistent disparities in financial need and access.

Our mission to help students attain career-accelerating first jobs is built on the foundation of college success, both in terms of accessibility and affordability. Improving our understanding of the challenges that underrepresented students face in affording, persisting, and completing college helps us strengthen our support of their future, long-term success. The high-level learnings in this memo are:

Higher education enrollment typically increases during recessions as the opportunity cost of attending college decreases. During the Great Recession, 4-year colleges saw a 6.1% year over year increase in enrollment, and 2-year colleges saw a 7.9% increase (7). Recession enrollment is typically characterized by high growth in adult students (aged 22 and older) (25) and growth in 2-year colleges and for-profit colleges (8).

However, COVID-19 is unique. Because of the uncertainty of the pandemic economy and the shift of the learning environment to be exclusively virtual, enrollment during COVID-19 is not following the patterns of past recessions (10).

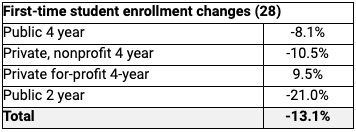

The Fall 2020 semester saw an overall decline in enrollment of 2.6%. The decline has been particularly acute for first-time undergraduate students whose enrollment declined by 13.1% though public 2-year schools had the greatest drop in enrollment.

All races saw a decline in enrollment (latest data from November 2020) though Black students saw the greatest decline at 7.5%. Hispanic students saw a 5.4% decline while white students saw a 6.6% decline. Across all races, men have seen disproportionate declines (e.g., -5.6% for Black males at public 4-year universities vs. -2.1% for Black females) (28).

Although not included in enrollment statistics, we do expect there was a drop in low-income students in the short term. ~100,000 fewer high school students completed FAFSA forms by the end of August 2020 as compared to the previous year. Similarly, educational research company EAB found that deposits from families with incomes below $60,000 to 100 4-year colleges were down 8.4% as of September 2020 (24).

Students from low and middle-income backgrounds were generally more likely to be negatively financially impacted by the pandemic. Although students were able to receive a reevaluation of their financial need requests at many colleges, many students and families may not have known this is an option (10). Last spring, at the start of the pandemic, McKinsey predicted that “in the virus-recurrence and pandemic-escalation scenarios, higher-education institutions could see much less predictable yield rates if would-be first-year students decide to take a gap year or attend somewhere closer to home (and less costly) because of the expectation of longer-term financial challenges for their families” (12).

It is clear that COVID-19 has impacted college persistence. In a Gallup survey of ~4,000 students pursuing a bachelor’s degree from September 22 – October 5, 2020, 49% of all respondents answered that it was “likely” or “very likely” that the COVID-19 pandemic would affect their ability to complete their bachelor’s degree. The number was even higher for Black and Hispanic students at 56% each (31).

The switch to online learning during COVID-19 is a key reason why persistence is at risk. Researchers at the University of Virginia studied persistence for Virginia’s community college students in the Spring 2020 semester and found that a shift to virtual instruction resulted in a 6.7 percentage point decrease in course completion. Furthermore, this effect was not mitigated if the instructor had experience teaching virtually (27).

Historical evidence shows that low-income students tend to be even more likely to withdraw from online courses relative to high-income peers (10). McKinsey anticipates that this trend will apply to the pandemic environment. They predict that low-income students’ persistence rates will decrease disproportionately as they are less likely to have the resources that enable success in an online learning environment (individual computers, high-speed internet, etc.). Furthermore, McKinsey noted that low-income students are more likely to face immediate financial challenges that impact their persistence as on-campus employment and other job opportunities decrease (12).

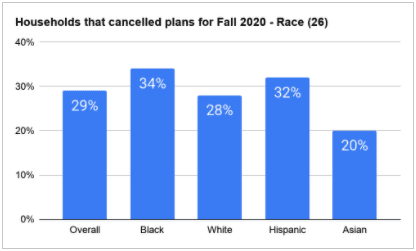

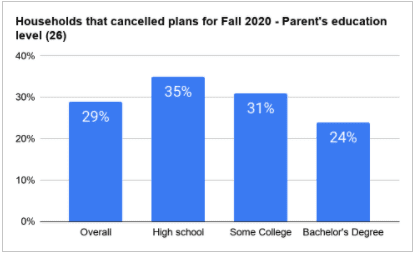

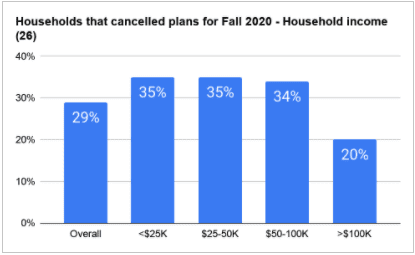

A US Census Survey polled households in mid-August with students at all levels of postsecondary education (non-credential program classes, certificate, associate’s degree, bachelor’s degree, graduate degree). They found that 29% of households with at least one expectant student canceled their fall enrollment plans (both new enrollment and returning enrollment). Black, Hispanic, low and middle-income, and first-generation households were most likely likely to cancel enrollment plans (26).

The top 3 reasons why students canceled plans were: uncertainty about online classes, concerns about getting COVID-19, and inability to pay for classes after a change in family financial circumstances. The uncertainty around online classes is particularly relevant to low-income students as they struggle to find a place to study or consistent access to high-speed internet. These early trends are particularly concerning as low-income students who “temporarily” stop attending school rarely return. Only 13% of college dropouts return and even fewer graduate (24).

There is early evidence of the disproportionate impact of COVID-19 on low-income students from the IZA Institute of Labor Economics and CUNY’s Queens College. Researchers found significant differences in educational, financial, and personal experiences between low-income students and the general population as a result of COVID-19. Low-income students were more likely to experience challenges attending online classes, have childcare responsibilities, lack internet, experience sickness, and feel overwhelmed. They were also 11% more likely to consider dropping a course due mostly to concerns that a poor grade would jeopardize their financial assistance. Finally, low-income students were 21% more likely to receive financial support (grants, stimulus payments, unemployment benefits) but were still at a higher risk of experiencing financial distress including securing basic food need, securing shelter, losing financial aid, and job loss (19).

College success cannot just be defined as enrolling in and graduating from college. Many also consider the financial cost to students of doing so (20). College cost and debt is particularly important for Braven as low-income and first-generation students are highly likely to borrow for college.

After a decade of rapid growth in annual borrowing, total federal loans have begun to decline – from $69.8B in 2013-2014 (in 2018 dollars) to $54.2B in 2018-2019, a 22% decrease (3). However, the decline has not been equal across all students. First-generation college students take out more student loans – and in higher amounts – than the general population (21) Furthermore, although the Pell Grant covered 79% of the cost of a public, 4-year university in 1975, today it only covers 28%. This drop has coincided with an increase in enrollment of students of color, who now have to find alternative ways to make up the Pell Grant gap (22).

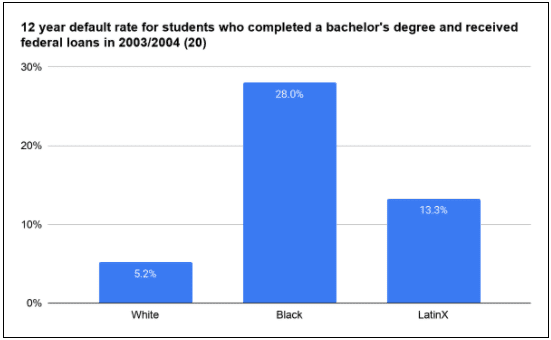

Among students who enrolled in a full-time bachelor’s degree program and completed their bachelor’s degree, 28% of Black students who received federal loans in 2003/2004 defaulted within 12 years. Comparatively only 5.2% of white students defaulted. The racial disparities are not the result of academic performance as data shows the GPAs of these graduates were relatively similar across races. The differences were most likely caused by 1) employment opportunities tied to the choice of majors, 2) institutional prestige, 3) financial assistance from families to help pay loans, and 4) racial discrimination in the labor market (20).

The disparate cost of education across race, household income, and first-generation status underscores the importance of Braven’s work to help college graduates put their education to work. The next memo will focus on labor market outcomes, how they are impacted by COVID-19, and what Braven can do to best prepare their student population to put their education to work.